Grain markets closed weaker today in choppy trade.

Corn was down 3 cents, KC wheat was 9 lower, MPLS wheat was

8 lower, CBOT wheat was a dime lower, Jan soybeans were down 2, the US Dollar

off 400 ticks or so with the March futures at 80.440, crude is at 97.50, gold

was off 22 bucks, and the DOW closed down 68 points.

Follow up selling for wheat today from the announcements the

past few days that include bigger crops in Australia and Canada. Plus no nearby issues for the wheat crop in

the U.S. It might not pencil out very

good for producers trying to make a profit but the market doesn’t seem to care

about that.

We did have export sales out this a.m. and considering it

was a holiday week last week they were not super bad but overall they were on

the disappointing side and didn’t help the bulls out at all today.

We did have corn and beans manage to get back to unchanged a

couple times during the session but when the markets closed they both ended in

the red.

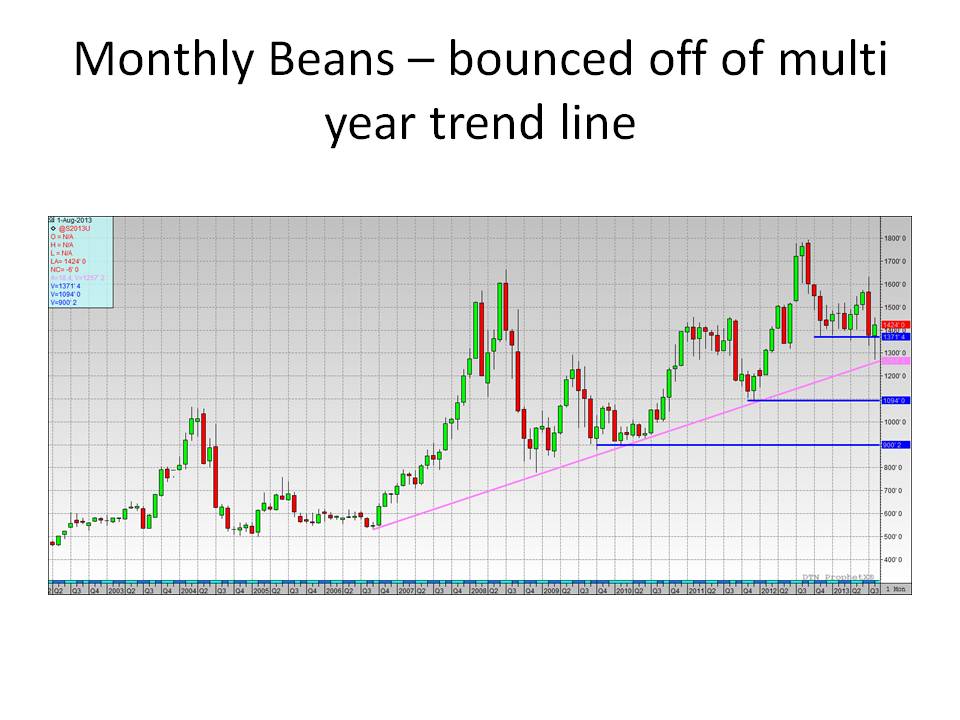

Technically you can find both some positives and negatives

when looking at the charts. You have some of the wheat charts back down

towards some major support that hopefully holds. But if it doesn’t it could really open up

further technical downside. You have soybean

charts that have moved a little range bound the past few days and corn charts

that had a very positive close early in the week. But today’s price action for corn opens up

the question as to was today a small breather/correction before moving higher

or have the last few days been a breather before resuming the selling pressure????

Only time will tell for sure and it probably depends on what

type of info the USDA puts out next week in their report.

Speaking of the report, CHS Hedging did release their pre-report

ideas for next week’s USDA report. Tim Emslie who is CHS Hedging Research Manager wrote up the comments for the

pre-report ideas; he along with DTN Senior Analyst Darrin Newsom are our two speakers for the

marketing meeting we are sponsoring this winter. It is in Pierre at the Ramkota at 10 a.m. on January 20th.

Here is the link to the info. https://www.chshedging.com/UserFiles/Documents/2013/Pre%20USDA%20Report%20Comments/120513.pdf

You will see that they are on the bandwagon of smaller

carryout numbers do to strong demand. But

how much of that demand is because of the season (harvest)? Also one needs to question what a couple

things are doing to demand. First off

what is the producer holding pattern doing to demand? Yes there is demand for products at present

price levels; but if the American Farmer doesn’t sell do the buyers find a

replacement of some sort?

How about the horrible freight/slow moving trains? As example I feel if mother nature would have

cooperated a little more and if trains would have showed up a little faster

that our elevators could have handled much more at harvest. But things didn’t come together………….will the

demand still be there later when the product wants to move is the question?

I have seen a few more orders pick up for the birdseed

industry; but overall things are still slow. We really need a little more demand.

Wheat basis, corn basis, and cash values in general seem to

be all over the board. I do like the

idea of having some offers out there because of how volatile freight and basis

is. It helps us know what type of

numbers we should be offering when we get someone looking to buy and that is worth

a lot for end users. To get coverage

without having to call 100’s.

Please give us a call if there is anything we can do for

you.

Thanks

Tony McDonald

Tony McDonald Carlos Aguilar

Carlos Aguilar DuPont Pioneer

DuPont Pioneer

Terry Johnston

Terry Johnston

Whitney McFerron

Whitney McFerron Emily Flory

Emily Flory Brennen Toquam

Brennen Toquam John Moore

John Moore OCJ & Ohio Ag Net

OCJ & Ohio Ag Net Ty Higgins

Ty Higgins Marcio Castelloes

Marcio Castelloes Karen Braun

Karen Braun Janice Kincheloe

Janice Kincheloe Mark Bernard

Mark Bernard Todd Calfee

Todd Calfee

Todd E. Gleason

Todd E. Gleason Aaron Combs

Aaron Combs Michael Hirtzer

Michael Hirtzer Paul Neiffer

Paul Neiffer Chris Narayanan

Chris Narayanan CHS Hedging Inc.

CHS Hedging Inc.